COMMENTARY:

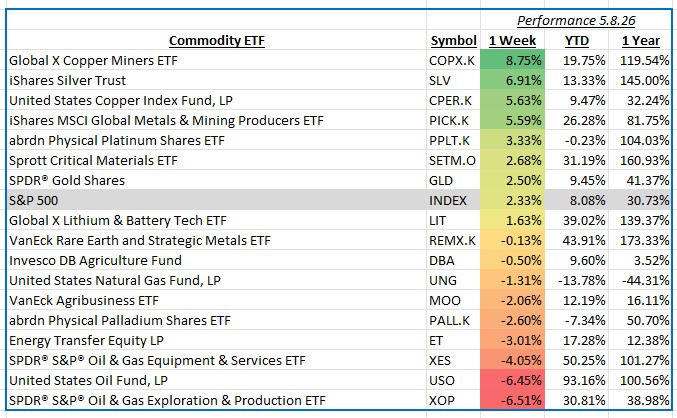

The S&P 500 advanced 2.33% for the week ending May 8, 2026, as investors responded positively to improving risk sentiment and stronger-than-expected corporate earnings across several growth-oriented sectors. Within the global commodities markets, investor attention remained focused on shifting demand expectations tied to global manufacturing activity, continued U.S. dollar weakness, and evolving supply conditions across energy and industrial metals markets. Industrial commodities benefited from renewed optimism surrounding infrastructure spending and artificial intelligence-related power demand, while precious metals gained support from lower real interest rates and increased expectations for future central bank easing.

Copper miners delivered the strongest performance among commodity-related exposures, rising 8.8% for the week as investors rotated aggressively into industrial metals tied to electrification, infrastructure, and artificial intelligence-related demand themes. Improving economic data from several large manufacturing economies, combined with ongoing supply constraints at key global mining operations, helped support higher copper prices during the week. Leading contributors included Freeport-McMoRan, First Quantum Minerals, and Southern Copper, which benefited from renewed optimism surrounding long-term copper demand growth tied to electric vehicles, power grids, and data center expansion.

Silver also posted strong gains, advancing 6.9% as precious metals rallied alongside improving industrial demand expectations and a softer U.S. dollar environment. Investor demand for hard assets increased as markets weighed the possibility of lower interest rates later this year. Silver producers and royalty companies outperformed broadly, led by strength in Pan American Silver, Wheaton Precious Metals, and Hecla Mining. The metal continued to benefit from its dual role as both a precious metal and an industrial input tied to solar energy and electronics manufacturing.

Metals and mining companies also generated strong returns, climbing 5.6% as broad commodity strength supported diversified miners and global materials producers. Investor sentiment improved following signs of stabilizing industrial activity and expectations for increased global infrastructure investment. Large diversified mining companies including BHP, Rio Tinto, and Glencore contributed meaningfully to sector gains as iron ore, copper, and other base metal prices strengthened during the week.

Oil, gas, and exploration companies were the weakest-performing commodity exposure, declining 6.5% as crude oil prices moved sharply lower amid concerns about slowing global demand growth and rising supply expectations. Energy markets reacted negatively to softer international economic data and uncertainty surrounding future production decisions from major exporting nations. Exploration and production companies were among the largest detractors, including weakness from Diamondback Energy, Devon Energy, and APA Corporation. Lower crude prices also pressured broader investor sentiment across the energy complex.

Overall, commodity markets reflected a growing divide between industrial and precious metals strength versus weakness in traditional energy markets. Investors continued to favor assets tied to electrification, infrastructure, and long-term industrial demand trends while remaining cautious toward areas exposed to slowing global energy consumption expectations.