COMMENTARY:

Global Commodities Market Commentary – Week Ending May 29, 2026

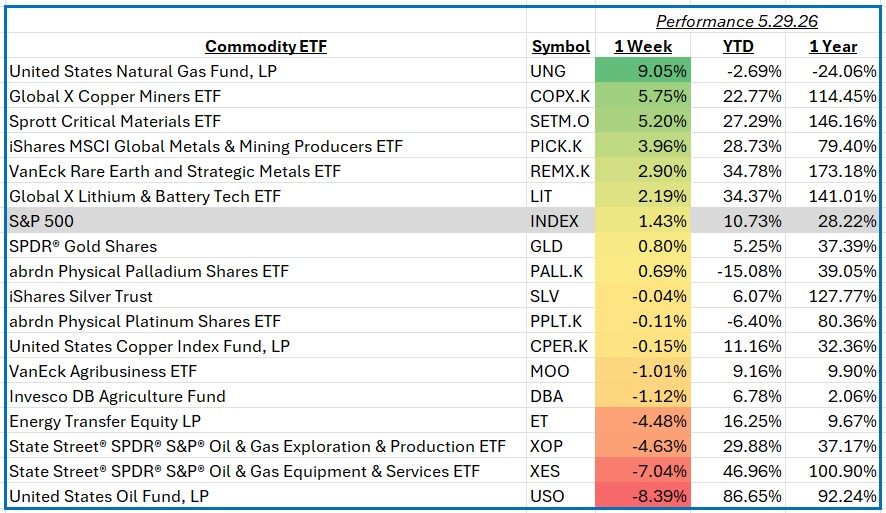

The S&P 500 advanced 1.43% for the week ending May 29, 2026, reflecting continued investor confidence in the economic outlook. Within global commodity markets, trading was influenced by several key themes, including shifting energy supply expectations, resilient industrial demand, and improving sentiment toward economically sensitive commodities. Investors also focused on signs of moderating inflation and the potential for lower interest rates later this year, which supported demand expectations across several commodity-linked sectors.

Natural Gas was the strongest-performing commodity exposure of the week, rising 9.0%. The rally was driven by forecasts for above-average summer temperatures, expectations for stronger electricity demand, and growing confidence that storage inventories will tighten as seasonal consumption increases. Companies tied to natural gas production and transportation benefited from the move higher, with notable contributions from EQT, Expand Energy, Williams Companies, and Kinder Morgan. Investors increasingly favored businesses positioned to benefit from improving natural gas fundamentals and growing long-term demand from power generation and export markets.

Copper Miners also delivered strong returns, gaining 5.8% for the week. Strength in copper prices reflected optimism surrounding global manufacturing activity, infrastructure spending, and accelerating electrification trends. Investor enthusiasm was further supported by expectations that artificial intelligence infrastructure, data center construction, and electric vehicle production will continue driving copper demand. Major contributors included Freeport-McMoRan, First Quantum Minerals, Southern Copper, and Lundin Mining. The sector benefited from both higher commodity prices and a favorable outlook for long-term industrial demand.

Crude Oil was the weakest-performing major commodity exposure, declining 8.4%. Prices came under pressure as markets evaluated the potential for increased global supply alongside concerns that demand growth may moderate in the second half of the year. The decline reflected a combination of profit-taking and changing expectations regarding future production levels. Lower crude prices weighed broadly on energy-related investments and reduced investor enthusiasm toward the sector during the week.

The broader Oil and Gas Value Chain, including exploration, production, equipment, and services companies, also struggled. Exploration and production businesses experienced the sharpest declines as lower oil prices pressured earnings expectations and cash flow projections. Significant contributors to weakness included ConocoPhillips, EOG Resources, Diamondback Energy, Devon Energy, and Occidental Petroleum. Oilfield services companies such as SLB, Halliburton, Baker Hughes, and TechnipFMC also moved lower as investors reassessed future drilling and capital spending activity. Despite the week’s weakness, many companies across the value chain continue to maintain strong balance sheets and disciplined capital allocation strategies.

Overall, commodity markets experienced a mixed week, with natural gas and industrial metals benefiting from improving demand expectations while energy markets faced pressure from declining crude oil prices. Investors remain focused on global growth trends, supply dynamics, and evolving monetary policy expectations as key drivers of commodity performance moving forward.