COMMENTARY:

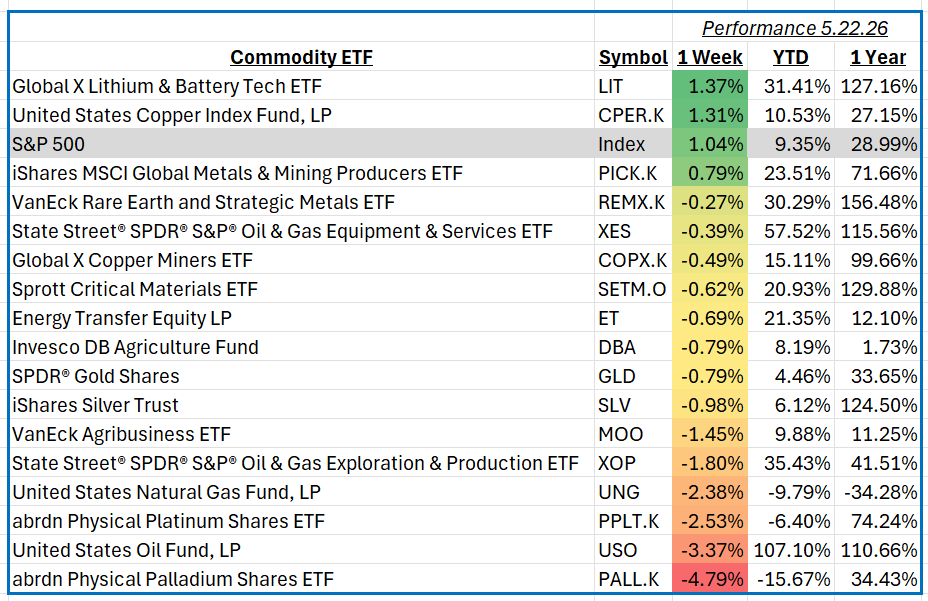

The S&P 500 advanced 1.04% for the week ending May 22, 2026, as investors responded positively to moderating inflation trends, resilient economic data, and continued strength in corporate earnings. Within the global commodities markets, attention remained focused on shifting expectations for global growth, supply discipline among major producers, and ongoing geopolitical developments affecting energy and industrial metals. Commodity markets were mixed overall, with investors balancing concerns about slowing manufacturing activity in parts of Europe and China against improving demand expectations tied to infrastructure spending, electrification, and artificial intelligence-related investment trends.

Lithium and battery technology was the strongest-performing commodity exposure for the week, gaining 1.4% as investors continued to favor companies leveraged to the global electrification theme. Improved sentiment surrounding electric vehicle demand and expectations for long-term battery storage growth supported the group. Large battery manufacturers and lithium producers were among the leading contributors, including Albemarle, Sociedad Química y Minera, Panasonic Holdings, and Tesla. Investors also reacted positively to expectations that supply growth may moderate following recent pricing weakness across lithium markets, helping stabilize outlooks for producers and battery supply chain companies.

Copper-related investments also posted solid gains, rising 1.3% during the week as industrial metals benefited from renewed optimism surrounding global infrastructure spending and artificial intelligence-driven power demand. Copper prices found support from tighter near-term inventories and expectations for stronger electricity grid investment globally. Major mining companies including Freeport-McMoRan, Southern Copper, BHP Group, and Glencore contributed positively to performance as investors continued to view copper as a key long-term beneficiary of electrification trends and energy transition spending.

Precious metals markets delivered mixed results during the week. Gold and silver prices remained relatively stable as moderating Treasury yields and persistent geopolitical uncertainty continued to support safe-haven demand. Several large precious metals miners and royalty companies helped stabilize returns across broader metals exposure. However, platinum group metals experienced significant weakness, with palladium declining 4.8% amid concerns about slowing global auto production and softer catalytic converter demand. Continued substitution toward platinum in automotive applications also pressured sentiment surrounding palladium producers and related mining companies.

Energy markets weakened notably during the week, with oil prices falling 3.4% as investors weighed concerns about slowing global demand growth and rising crude inventories. Softer economic data from China and ongoing uncertainty surrounding global manufacturing activity contributed to the decline. Oil service companies and exploration producers faced pressure as lower crude prices reduced near-term enthusiasm for upstream spending growth, despite continued supply discipline from major exporting nations.

Overall, commodity markets reflected a cautious but constructive tone this week as investors balanced slowing global growth concerns against long-term structural demand themes tied to electrification, infrastructure investment, and energy security.