COMMENTARY:

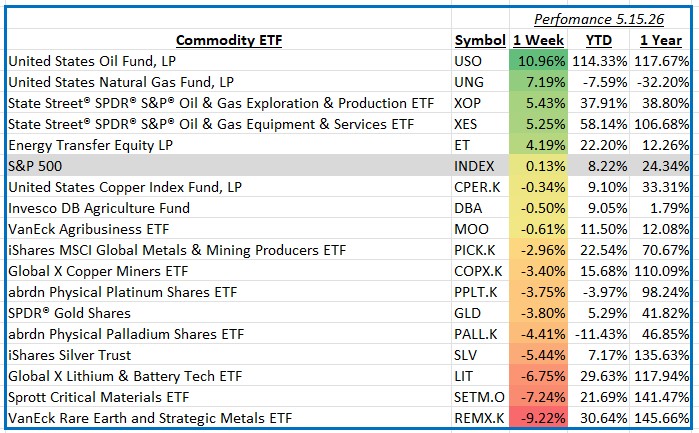

The S&P 500 eked out a modest gain of 0.13% for the week ending May 15, 2026, masking a significant divergence playing out beneath the surface — one defined almost entirely by the global energy crisis. The continued closure of the Strait of Hormuz, through which roughly 35% of the world’s seaborne crude oil trade normally flows, kept energy markets on edge throughout the week. The International Energy Agency warned that global oil markets could remain severely undersupplied through October, even if hostilities ease in the near term. Meanwhile, a Trump-Xi summit in China concluded without major agreements, doing little to ease market anxieties around inflation and global trade.

Crude Oil — Top Performer (+10.9%) Crude oil was the standout commodity of the week by a wide margin, surging nearly 11% as WTI futures climbed toward $106 per barrel. The driver was straightforward: the Strait of Hormuz remained effectively closed, with tanker traffic through the Persian Gulf at minimal levels and Middle Eastern production from countries including Iraq, Saudi Arabia, and Kuwait still sharply curtailed. The United States Oil Fund, which tracks front-month WTI futures contracts, captured this move in full. With no equity holdings, performance reflected the raw commodity price directly. Stalled peace talks between the U.S. and Iran — punctuated by President Trump’s warning of “annihilation” if a deal was not reached — further elevated the risk premium embedded in crude prices.

Natural Gas — Strong Performer (+7.2%) Natural gas followed crude higher, gaining 7.2% for the week. Iran’s South Pars field, the world’s largest natural gas reserve, has been disrupted by the conflict, removing a meaningful source of global LNG supply. The United States Natural Gas Fund, which holds near-term natural gas futures contracts, tracked this move closely. Domestic production from U.S. shale basins remained steady near 104 billion cubic feet per day, but growing LNG export demand — fed by new capacity at Gulf Coast terminals — continued to tighten the domestic balance. AI-driven data center electricity demand added a structural tailwind to the price story.

The Broader Oil and Gas Value Chain (+5.3% to +5.4%) The strength in commodity prices cascaded across the entire oil and gas value chain. Exploration and production companies benefited directly from the higher price environment, with equal-weighted exposure across independent producers amplifying returns relative to large-cap benchmarks. On the equipment and services side, names involved in drilling, well servicing, and production support saw increased investor interest as expectations grew that elevated prices would eventually spur incremental spending and activity. Companies such as Schlumberger, Halliburton, and Baker Hughes — all prominent holdings — contributed meaningfully to the gains across this part of the value chain.

Rare Earth and Strategic Metals — Laggard (−9.2%) The week’s sharp loser was the rare earth and strategic metals space, which fell 9.2% — a dramatic reversal from recent strength. The fund tracking this theme holds a significant weight in lithium-focused names, and that exposure proved costly. Albemarle, the world’s largest lithium producer and the fund’s top holding, came under pressure alongside fellow lithium miners Pilbara Minerals, Ganfeng Lithium, and SQM, as lithium prices remained depressed amid persistent oversupply. Lynas Rare Earths, the largest ex-China rare earth producer, also declined. Broader risk-off sentiment tied to the unresolved Middle East conflict and inflation concerns weighed on the sector, which had already begun showing technical signs of exhaustion after a strong run earlier in the year.

It was a week defined by the geography of energy. The persistent closure of the Strait of Hormuz elevated commodity prices across the board, rewarding investors with energy exposure while punishing those positioned in rate-sensitive and growth-dependent materials. With geopolitical uncertainty showing no signs of quick resolution and inflation pressures building, markets are likely to remain volatile as investors continue weighing the implications of a prolonged energy supply shock.