COMMENTARY:

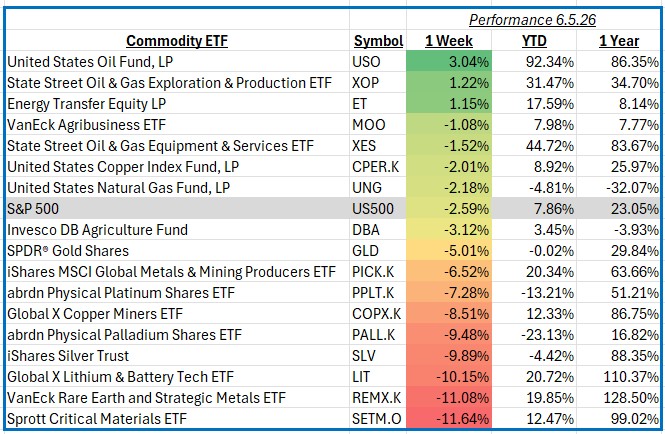

The S&P 500 Index declined 2.59% for the week ending June 5, 2026, as investors weighed slowing economic growth expectations against ongoing inflation concerns and uncertainty surrounding future monetary policy. Within global commodity markets, performance was mixed, with energy-related exposures benefiting from stronger crude oil prices while industrial and strategic minerals experienced significant weakness. Key market themes included renewed strength in oil markets, resilient energy infrastructure demand, and continued concerns regarding global manufacturing activity and electric vehicle supply chains.

Oil was the strongest-performing commodity exposure during the week, advancing 3.0%. Crude prices moved higher as investors responded to tightening global supply expectations, geopolitical risks, and signs of resilient seasonal fuel demand. The strength in oil prices supported companies throughout the energy value chain, particularly integrated producers and refiners. Major contributors included Exxon Mobil, Chevron, ConocoPhillips, and Occidental Petroleum, which benefited from improving commodity price expectations and strong free cash flow generation.

Oil and Gas Exploration also delivered positive returns, gaining 1.2% during the week. Exploration and production companies outperformed as higher crude prices translated directly into improved earnings expectations. Investors favored businesses with strong reserve bases and disciplined capital spending programs. Leading contributors included EOG Resources, Diamondback Energy, Devon Energy, and APA Corporation, all of which benefited from their sensitivity to rising oil prices and favorable production outlooks.

Energy Transfer-related infrastructure exposure also advanced 1.2%, reflecting the defensive characteristics of midstream energy businesses. Pipeline operators and storage companies continued to benefit from stable volumes, attractive dividend yields, and long-term contractual cash flows. Key contributors included Energy Transfer, Enterprise Products Partners, The Williams Companies, and Kinder Morgan. Investor demand for income-oriented assets remained supportive as market volatility increased elsewhere.

The weakest area of the commodity value chain was Critical Minerals, which declined 11.6%. Strategic and technology-focused metals were pressured by concerns surrounding global industrial demand, slowing manufacturing activity, and uncertainty regarding electric vehicle adoption rates. Companies involved in rare earth processing and advanced materials production experienced significant selling pressure as investors reduced exposure to economically sensitive growth themes.

Rare Earth and Strategic Metals fell 11.1%, while Lithium declined 10.2% for the week. Lithium producers and battery-material suppliers continued to face pressure from lower commodity prices and concerns about oversupply in key markets. Major detractors included Albemarle, Sociedad Química y Minera de Chile (SQM), Arcadium Lithium, MP Materials, and Lynas Rare Earths. Weak sentiment across battery materials and strategic metals weighed heavily on the broader clean-energy supply chain despite favorable long-term demand trends.

Overall, commodity markets reflected a clear divide between traditional energy and energy-transition materials. Strength in crude oil and energy infrastructure helped offset weakness in strategic minerals and battery metals, highlighting investors’ preference for near-term cash flow and earnings visibility. As markets move forward, commodity investors will continue monitoring global growth trends, supply dynamics, and geopolitical developments for direction.