COMMENTARY:

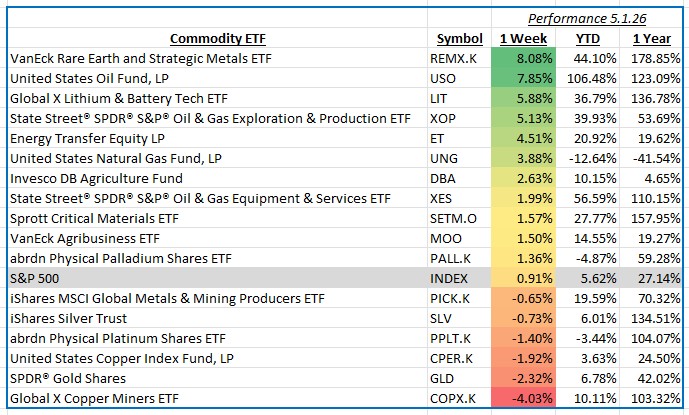

The S&P 500 gained 0.91% for the week ending May 1, 2026, as investors navigated another active stretch for global commodity markets. Rising geopolitical tensions surrounding the Strait of Hormuz pushed energy prices sharply higher, while improving sentiment toward artificial intelligence infrastructure and global electrification trends continued to support select mining and battery-related industries. Commodity markets also reacted to resilient U.S. economic data, steady global demand expectations, and ongoing concerns surrounding supply chain disruptions in key resource-producing regions.

Earth and strategic minerals delivered the strongest performance of the week, advancing 8.1% as investors focused on growing demand for rare earth materials tied to electric vehicles, renewable energy systems, and defense technologies. The group benefited from renewed optimism surrounding China’s industrial outlook and tighter supply expectations across several specialty metals markets. Leading contributors included MP Materials, Lynas Rare Earths, and China Northern Rare Earth Group, as investors positioned for long-term structural demand tied to global electrification and advanced manufacturing initiatives.

Oil-related investments also posted strong gains, rising 7.9% during the week as crude prices climbed on concerns surrounding potential supply disruptions in the Middle East. Reports tied to shipping constraints near the Strait of Hormuz and stronger U.S. export activity helped support energy markets throughout the week. Large integrated producers and exploration companies, including Exxon Mobil, Chevron, and ConocoPhillips, were among the largest contributors as investors favored companies with strong cash flow generation and direct leverage to rising oil prices.

Lithium battery technology exposure advanced 5.9% as enthusiasm around electric vehicle production and energy storage demand remained constructive. Investors responded favorably to continued investment in battery supply chains and improving sentiment toward long-term clean energy adoption. Tesla, Albemarle, Panasonic Holdings, and BYD were among the strongest contributors, while semiconductor and battery component suppliers also supported overall sector gains during the week.

Copper miners lagged the broader commodity complex, declining 4.0% as weaker copper prices and concerns surrounding slowing industrial activity weighed on sentiment. Investors remained cautious around construction demand trends in China and Europe, leading to profit-taking across diversified mining companies. Freeport-McMoRan, First Quantum Minerals, and Southern Copper were among the largest detractors as lower metals pricing offset otherwise stable long-term demand expectations tied to infrastructure and electrification spending.

Overall, commodity markets experienced another volatile but constructive week, with energy and strategic minerals leading gains while industrial metals faced pressure from growth concerns. Investors continue to balance geopolitical developments, inflation trends, and long-term demand themes tied to global infrastructure and energy transition investments.