COMMENTARY:

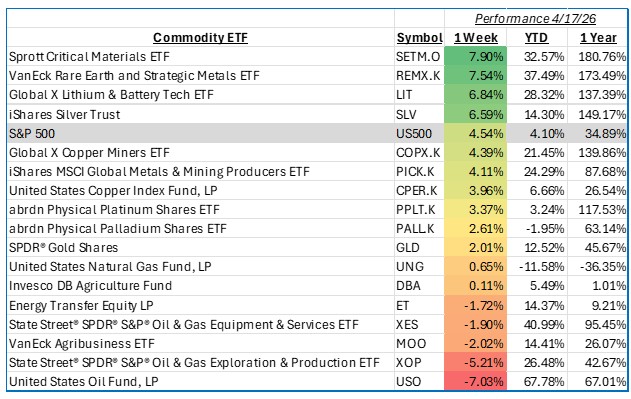

The S&P 500 delivered a strong performance this week, advancing 4.54% for the period ending April 17, 2026, as investor sentiment improved across risk assets. Within global commodities, markets were shaped by a combination of easing macro concerns, a weaker U.S. dollar, and renewed focus on supply constraints. Notably, industrial and strategic metals outperformed amid growing demand tied to electrification and energy transition themes, while energy markets faced pressure from shifting supply dynamics and softer demand expectations.

The standout performer this week was the critical minerals segment, which posted a 7.9% gain. Strength in this area was driven by increasing global investment in battery supply chains and supportive policy signals from major economies aimed at securing domestic sources of key inputs. Performance was led by companies with exposure to lithium, nickel, and cobalt production, as well as processors benefiting from tightening supply conditions. Several mid- and large-cap names tied to electric vehicle infrastructure and battery materials were primary contributors, reflecting strong investor interest in long-term structural demand trends.

Similarly, rare earth and strategic minerals delivered an impressive 7.5% return over the week. Gains were fueled by geopolitical developments and ongoing concerns about concentrated global supply, particularly from dominant exporting nations. Companies involved in rare earth extraction and processing saw notable upside, alongside firms positioned in downstream applications such as magnet manufacturing. The rally was broad-based, with both established producers and emerging developers contributing meaningfully as markets priced in the importance of supply chain diversification.

In contrast, the oil sector lagged significantly, declining 7.0% for the week. Crude prices came under pressure due to a combination of rising inventories, easing geopolitical tensions, and indications of stable to increasing production from key exporting countries. Integrated oil majors and exploration and production companies were the primary detractors, with weaker realized pricing weighing on earnings expectations. Oilfield services names also faced headwinds as activity outlooks softened marginally alongside declining price momentum.

Elsewhere across commodities, precious metals saw moderate gains supported by lower real yields and a softer dollar, while base metals benefited from improved growth sentiment. Agricultural markets were mixed, with weather patterns and shifting export dynamics influencing price action. Broadly, commodity-linked equities reflected a rotation toward future-facing resources tied to electrification, while traditional energy exposures lagged.

In summary, this week highlighted a clear divergence within commodities, as investors favored strategic and critical materials aligned with long-term demand themes while rotating away from conventional energy. Market momentum remains constructive, though sector dispersion suggests continued selectivity will be key in the weeks ahead.