Gold & industrial metals delivered very different flavors of upside in 2025, and that split sets up a clear choice for 2026 positioning.

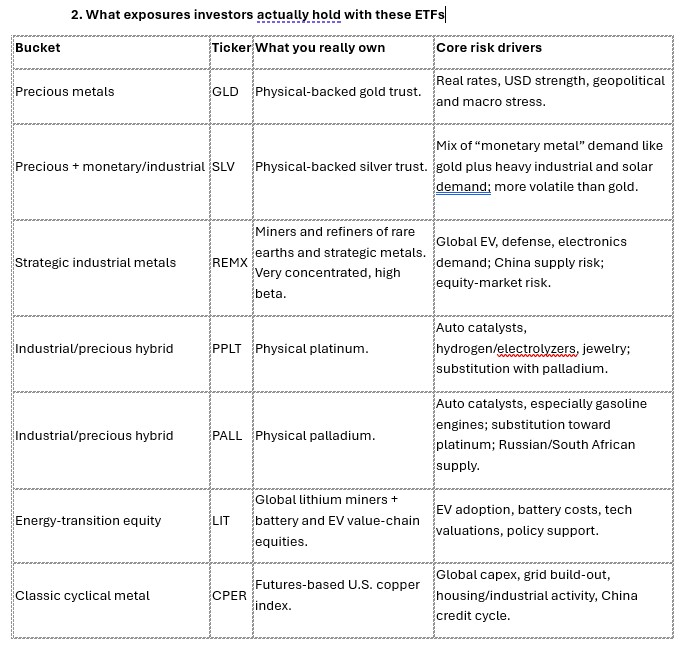

- 2025 scorecard – precious vs industrial

Precious metals

- GLD (gold): Gold had a huge year; GLD returned about 64% in 2025, beating major equity indices as investors looked for safety amid political and macro uncertainty.

- SLV (silver): Silver did even better; estimates put silver gains around 95% in 2025, with silver prices beating gold and the S&P 500 on a mix of industrial shortages, falling inventories, and monetary‑policy shifts.

Industrial / strategic metals

- REMX (rare earth & strategic metals): REMX delivered roughly 90–100% total return in 2025, more than doubling as demand for rare earths and battery/EV inputs surged.

- LIT (lithium & battery tech): Also participated in the metals‑plus‑electrification trade, with strong 2025 performance tied to EV and storage demand; it shows up on “hottest ETFs of 2025” lists, though with more stock‑specific and tech risk than pure metal trusts.

- PPLT (platinum) & PALL (palladium): Both benefited from precious‑plus‑industrial use (auto catalysts, hydrogen, electronics), but lagged the blow‑out moves in gold, silver, and rare earths; returns were positive but not market‑leading in 2025.

- CPER (U.S. copper): Copper rode the global growth and energy‑transition story, with solid double‑digit 2025 gains but again overshadowed by the parabolic moves in silver and rare earths.

- What to think about in 2026.

Given how extreme 2025 was, the central question is: who can still surprise on the upside without simply round‑tripping last year’s gains?

Case for precious metals (GLD, SLV)

- Gold’s 64% run in 2025 means expectations are now high, but the macro drivers—high debt, sticky inflation, periodic risk‑off shocks—haven’t gone away, which supports a floor under GLD.

- Silver combines that macro hedge with secular solar and electronics demand; its 2025 outperformance shows how tight inventories already are.

Risk: both GLD and SLV could consolidate or correct if real yields rise or risk sentiment improves, especially after such a strong year.

Case for industrial/transition metals (REMX, LIT, CPER, PPLT, PALL)

- REMX’s 92%+ 2025 gain came from a narrow group of rare‑earth and strategic‑metal names; momentum and a 2026 YTD gain over 30% show the theme is still in favor.

- Policy and supply constraints support copper and battery metals: grid build‑out, EV adoption, data‑center power demand, and defense spending all pull on the same supply‑constrained metals stack.

- Platinum and palladium can benefit if auto production stays robust and if stricter emissions or hydrogen‑economy spending ramps up, but they are more niche and dependent on automaker behavior.

** This is NOT investment advice, the comments are for educational purposes only