COMMENTARY

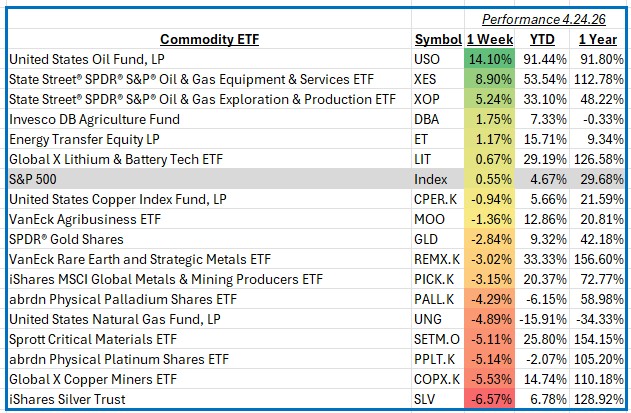

The S&P 500 advanced 0.55% for the week ending April 24, 2026, supported in part by a sharp rebound across global commodities markets. Energy prices led the move higher, while metals showed more mixed performance. Key macro highlights included tightening crude supply expectations driven by geopolitical developments, improving demand signals from major economies, and continued volatility in precious metals as interest rate expectations shifted alongside currency movements.

Across commodities, performance was driven by a combination of supply-side constraints and evolving demand outlooks. Oil markets tightened meaningfully, while industrial and battery-related materials remained supported by long-term electrification trends. In contrast, precious metals faced pressure from a stronger U.S. dollar and rising real yields, underscoring the importance of macro drivers in shaping short-term price action.

Oil was the standout performer, surging 14.1% for the week. The rally was fueled by renewed supply concerns, including production discipline among major exporters and geopolitical risks that elevated risk premiums. Strength was reflected across integrated majors and upstream producers, with companies such as Exxon Mobil, Chevron, and ConocoPhillips contributing significantly to gains. Improved refining margins and stronger forward pricing also supported sentiment across the complex.

Oilfield services and equipment, along with exploration and production, also posted strong gains of 8.9% and 5.2%, respectively. This performance reflected rising capital expenditure expectations as higher oil prices incentivized increased drilling activity. Leading contributors included Schlumberger, Halliburton, and Baker Hughes, all of which benefited from improving utilization rates and pricing power. Upstream producers similarly gained on stronger cash flow outlooks and disciplined production growth strategies.

Silver lagged the broader commodities complex, declining 6.8% for the week. The weakness was driven by a combination of rising real interest rates and a firmer U.S. dollar, both of which tend to pressure precious metals prices. Major contributors to the downside included companies such as Pan American Silver and First Majestic Silver, as well as diversified miners with silver exposure. Industrial demand signals remained stable, but were overshadowed by macro headwinds.

Overall, the week highlighted a clear divergence within commodities, with energy leading on supply-driven dynamics while precious metals lagged under macro pressure. Markets continue to reflect a balance between cyclical recovery and evolving monetary expectations.